Winter Camp Budgeting: What No One Tells You About Hidden Risks

Sending your kid to winter camp? I did—twice—and almost got burned. It’s not just about tuition; it’s the surprise costs, refund traps, and payment plans that nobody warns you about. I learned the hard way. Now, I’m sharing what really matters: spotting financial risks before they snowball. This isn’t just budgeting—it’s risk-smart parenting. Let’s walk through the real game behind winter camp spending. Behind the cheerful flyers and glowing testimonials lies a financial landscape few parents fully understand. The excitement of enrolling a child in a seasonal program often overshadows the quiet, compounding risks that can strain household budgets. From non-refundable deposits to last-minute supply fees, the true cost of participation goes far beyond the advertised price. This article unpacks those hidden layers, offering a clear-eyed look at what families face—and how to plan with confidence.

The Allure and Pressure of Winter Camps

Winter camps are often marketed as essential experiences for children’s development, promising enrichment, social engagement, and safe supervision during school breaks. For many parents, especially working mothers managing household schedules, these programs appear to be a practical solution to the challenge of winter vacation childcare. The appeal is understandable: structured days, educational activities, and the reassurance that children are engaged in meaningful ways while parents maintain their professional responsibilities. Brochures highlight smiling kids building snow forts, learning science experiments, or creating holiday crafts—images that evoke warmth, growth, and joy.

Yet beneath this polished presentation lies a powerful emotional current that influences decision-making. Social pressure plays a significant role. When neighbors, friends, or school parents mention their children’s camp plans, it can create a sense of urgency or even guilt. The fear of missing out—on social integration, developmental opportunities, or simply peace of mind—can push families toward enrollment even when finances are stretched. This emotional pull is amplified by targeted advertising that frames camps as investments in a child’s future, subtly suggesting that opting out may put a child at a disadvantage.

Marketing strategies often emphasize exclusivity, limited spots, or early registration bonuses, all designed to accelerate decisions. Phrases like “secure your child’s spot today” or “spaces filling fast” trigger scarcity bias, a well-documented psychological tendency to act quickly when opportunities seem scarce. These tactics are effective because they tap into parental instincts to provide the best for their children. However, when emotion overrides financial caution, families may commit to expenses without fully evaluating affordability or long-term impact.

The pressure is especially acute for single-income households or families navigating tight budgets. In these cases, the perceived necessity of winter camp can overshadow alternative options that are equally enriching but less costly. Community centers, libraries, or informal neighborhood groups often offer free or low-cost activities during school breaks, yet they receive less visibility and social validation. As a result, parents may feel that choosing these alternatives reflects a compromise in quality or care, even when the educational and social benefits are comparable. Recognizing these psychological and social influences is the first step toward making intentional, financially sound choices.

Breaking Down the True Cost Structure

When parents first review a winter camp’s brochure, the tuition fee is typically the most visible number. It’s often presented as a flat weekly rate, making it easy to assume that this is the total cost. But in reality, tuition is only the beginning. The full financial picture includes a range of additional expenses that can significantly increase the final bill. These hidden costs—transportation, gear, meals, activity add-ons, and insurance—are rarely highlighted in promotional materials, leaving families unprepared for the actual outlay.

Transportation is one of the most overlooked expenses. While some camps offer bus services, these often come with extra fees that vary by distance and frequency. For families without access to such services, the cost of daily drop-offs and pickups must be factored in, including fuel, vehicle wear, and time. In urban areas, public transit may be an option, but it still represents a recurring expense. For those living farther from camp locations, weekend boarding options might be available, but these usually carry a premium price tag that can double the base tuition.

Another major cost category is required gear or uniforms. Many winter camps, particularly those focused on outdoor or specialty activities like skiing, robotics, or theater, mandate specific equipment. Parents may be asked to purchase insulated boots, snowsuits, safety goggles, or technical tools—all of which can add hundreds of dollars to the total. In some cases, gear is non-negotiable and must meet exact specifications, leaving little room for secondhand alternatives. Even when used items are allowed, the initial investment remains substantial, and replacement costs can arise if items are lost or damaged during camp.

Meal plans are another layer of expense. While some camps include lunch and snacks in the tuition, others operate on an opt-in basis, charging extra for daily meals. Dietary accommodations, such as gluten-free or nut-free options, may incur additional fees. For children with specific nutritional needs, parents may end up packing food anyway, but the lack of transparency about meal inclusions can lead to unexpected charges upon registration. Similarly, activity add-ons—such as field trips, guest workshops, or extended-day programs—are often marketed as optional enhancements but can quickly become expected components of the camp experience.

Insurance is a less visible but important consideration. Some camps require families to purchase supplemental accident or medical coverage, particularly for high-risk activities. These policies may cost $50 to $100 per week and are typically non-refundable. While the intent is to protect participants, the added cost is another financial burden that must be weighed against the overall value of the program. When all these elements are combined, the true cost of winter camp can easily exceed the advertised tuition by 30% to 50%, a reality that many families only discover after committing.

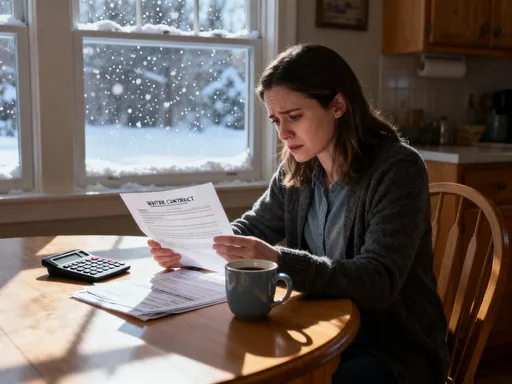

Hidden Risks in Payment and Refund Policies

Many winter camps offer flexible payment plans to make enrollment seem more accessible. Monthly installments, early-bird discounts, or sliding-scale fees can make the financial commitment appear manageable. However, these plans often come with strict conditions that favor the provider over the consumer. The real risk emerges when unforeseen circumstances—such as illness, job loss, or family emergencies—make attendance impossible. In such cases, families may find themselves locked into non-refundable agreements that offer little to no flexibility.

Refund policies are where the most significant financial risks lie. Some camps state clearly that deposits are non-refundable, while others impose rigid cancellation timelines. For example, a common clause might read: “No refunds issued within 30 days of the start date.” This means that even if a child falls ill a week before camp begins, the full fee may still be forfeited. In more extreme cases, camps do not offer refunds for weather-related closures, medical emergencies, or family relocations. These terms are often buried in lengthy enrollment agreements, presented in dense legal language that discourages thorough reading.

Another red flag is the use of non-transferable fees. Even if a sibling could attend in place of the enrolled child, some camps prohibit name changes or transfers, rendering the payment useless. This lack of flexibility can be especially painful when a child decides at the last minute not to participate or becomes too anxious to attend. In such situations, parents are left with no recourse and no recovery of funds, despite having made the decision in good faith.

Payment plans themselves can create additional risk. While spreading the cost over several months may ease cash flow, it can also create a false sense of affordability. Families may overlook the total amount being committed, focusing instead on the monthly installment. If a financial setback occurs—such as a reduction in income or an unexpected expense—the obligation to continue payments can become a serious burden. Some plans include interest or administrative fees, further increasing the total cost. Understanding these terms before signing is critical to avoiding financial strain.

To protect themselves, parents should treat enrollment like any major purchase: read the fine print, ask questions, and seek clarification on ambiguous terms. Key questions include: What happens if my child cannot attend due to illness? Can I transfer the spot to another family member? Are there any exceptions to the refund policy? If the answers are unclear or unsatisfactory, it may be wise to consider alternative programs with more transparent and family-friendly policies.

The Opportunity Cost of Overspending on Camps

Every dollar spent on winter camp is a dollar not allocated to other financial priorities. This concept, known as opportunity cost, is often overlooked in the heat of enrollment season. While the immediate benefit of camp—childcare, enrichment, fun—is tangible, the long-term cost of diverting funds from savings, investments, or emergency reserves can be substantial. For families already balancing tight budgets, overspending on seasonal programs can delay progress toward more critical goals, such as building an emergency fund, saving for college, or paying down high-interest debt.

Consider a family that spends $1,200 on a two-week winter camp. That amount, if invested conservatively at a 5% annual return, could grow to over $3,000 in ten years. Alternatively, it could cover three months of groceries, a major home repair, or a significant portion of a child’s college textbook expenses. When viewed through this lens, the decision to spend becomes not just about the camp’s value, but about what is being sacrificed to afford it. The trade-off is rarely discussed in marketing materials, yet it lies at the heart of sound financial planning.

Moreover, repeated seasonal spending—on winter camp, summer camp, holiday programs, and extracurriculars—can create a pattern of financial leakage. Small, recurring expenses that seem manageable in isolation can accumulate into a significant drain over time. A family that spends $1,000 each season on enrichment programs is effectively spending $4,000 annually—more than the average American saves in a year. Over five years, that totals $20,000, a sum that could fund a down payment on a car, a home renovation, or a substantial retirement contribution.

The key is to evaluate whether a camp delivers value beyond entertainment. Does it offer unique educational benefits that are not available at home or in the community? Does it fill a genuine childcare need, or is it primarily a convenience? Is the cost proportionate to the benefit received? These questions help shift the focus from emotional desire to strategic evaluation. By measuring camp spending against long-term financial health, families can make choices that align with their broader goals rather than short-term impulses.

Risk Assessment: A Practical Framework for Parents

Deciding whether a winter camp is worth the investment requires more than a gut feeling. A structured risk-assessment approach can help parents move from emotional decision-making to informed judgment. This framework evaluates four key factors: cost transparency, flexibility, educational value, and alignment with family goals. Each component provides insight into the program’s true worth and potential financial exposure.

Cost transparency refers to how clearly and completely the camp discloses all fees. A high-scoring program will provide a detailed breakdown of tuition, supplies, transportation, and optional add-ons upfront. Low transparency—such as vague descriptions or hidden charges revealed late in the process—signals higher financial risk. Parents should be wary of programs that require additional payments after registration or that do not publish a full price list.

Flexibility measures how accommodating the camp is in the face of life’s uncertainties. Does it offer pro-rated refunds? Can enrollment be transferred or deferred? Are there options for partial attendance or makeup days? A flexible program recognizes that families face unpredictable challenges and builds in safeguards to protect them. In contrast, rigid policies increase the likelihood of financial loss due to circumstances beyond the family’s control.

Educational value assesses what the child gains beyond supervision. Is the curriculum structured and age-appropriate? Are there qualified instructors and measurable learning outcomes? Programs that emphasize skill development, creativity, or social-emotional growth tend to offer higher value than those focused solely on recreation. However, value must be weighed against cost—no program should be considered “worth it” simply because it sounds impressive.

Finally, alignment with family goals ensures that the camp supports the household’s broader priorities. For some families, the primary need is reliable childcare; for others, it’s academic enrichment or physical activity. A camp that aligns with these objectives is more likely to deliver meaningful benefits. Using this framework, parents can score potential programs and compare options objectively, reducing the influence of marketing pressure and emotional appeal.

Smarter Alternatives and Cost-Saving Tactics

Enrichment does not have to come with a premium price tag. Families can access meaningful experiences through lower-cost, lower-risk alternatives that provide similar benefits without the financial strain. Community programs, local workshops, library events, and neighborhood co-ops often offer structured activities during school breaks at little or no cost. These options may lack the branding of private camps, but they frequently deliver comparable social and educational value.

Local recreation departments, religious organizations, and nonprofit groups regularly host winter break programs that include arts and crafts, games, homework help, and outdoor play. Many are staffed by trained professionals and operate on sliding-scale fees based on income. Some even offer scholarships or sponsorships for families in need. These programs may not include exotic field trips or specialized equipment, but they provide safe, engaging environments where children can learn and connect with peers.

Cost-saving tactics within traditional camps can also make a difference. Early-bird registration often comes with discounts of 10% to 20%, making it worthwhile to plan ahead. Sibling discounts are another common perk—some camps reduce the second child’s fee by 15% or more. Families should also inquire about referral bonuses, group rates, or nonprofit partnerships that could lower costs. In some cases, direct negotiation is possible; while not all camps are open to bargaining, smaller or independent programs may be willing to adjust fees for committed families.

Pooling resources with other parents through co-op childcare is another effective strategy. A group of families can take turns supervising children at home, rotating responsibilities and sharing the cost of activities. This approach fosters community, reduces isolation, and preserves financial flexibility. It also allows for more personalized programming tailored to children’s interests, from cooking classes to science experiments to movie days.

The goal is not to eliminate camp entirely, but to make informed choices that balance value, cost, and risk. By exploring alternatives and applying smart tactics, families can enjoy the benefits of winter break enrichment without compromising their financial stability.

Building Financial Resilience Beyond the Season

Winter camp is more than a seasonal expense—it’s a reflection of a family’s overall financial health. The decisions made around enrollment reveal deeper habits around budgeting, risk management, and long-term planning. By treating camp spending as part of a larger financial picture, families can build resilience that extends far beyond the winter months. The key is proactive preparation: setting aside funds months in advance, creating emergency buffers, and establishing clear spending priorities.

One effective strategy is to open a dedicated savings account for seasonal expenses. By contributing small amounts regularly—such as $50 per month—families can accumulate $600 by winter, enough to cover a modest camp fee or reduce reliance on payment plans. Automating these transfers ensures consistency and removes the burden of last-minute scrambling. This approach not only eases cash flow but also reinforces disciplined financial behavior.

Equally important is maintaining an emergency fund. Financial experts recommend saving three to six months’ worth of living expenses to handle unexpected setbacks. When such a cushion exists, families are less likely to feel pressured into rigid payment agreements or to sacrifice essentials to cover camp costs. Knowing that a backup plan is in place allows for more confident, less stressful decision-making.

In the end, avoiding financial risk is not about cutting corners or denying children enriching experiences. It’s about making smarter, informed choices that protect the family’s future. Winter camp can be a valuable opportunity—but only when it fits within a thoughtful, sustainable financial plan. By focusing on transparency, flexibility, and long-term goals, parents can navigate the season with confidence, knowing they’ve made choices that support both their children’s growth and their household’s stability.